Understanding Your Situation

Transparent Finances First

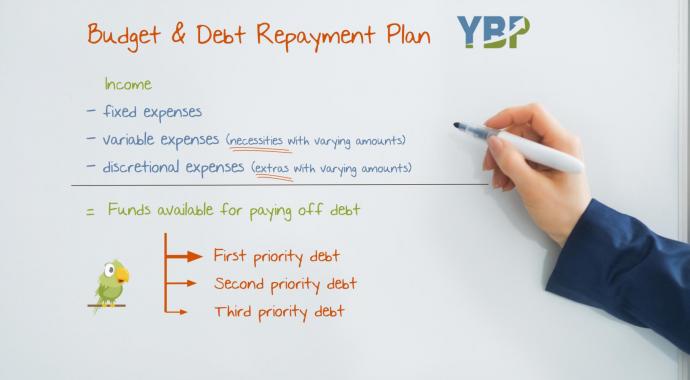

When discussing debt reduction, it is hard to know just how to pay off the debt without knowing how much income there is versus how much debt there is. So, the first things to do are:

- To make a budget and figure out how much is spent on fixed costs, then variable costs, then discretionary costs.

- List all of the bad debt (unplanned) that needs repayment asap to reduce the worry level.

- Use this information to create a repayment plan that you can stick to.

- Follow the budget and the payment plan. It is no use creating a repayment plan only to go out and spend more than can be paid back.

Consider the Reasons

So now you're good to start because you've got the numbers figured out, right?

Almost, but not fully. As important as knowing your expenses and income, is figuring out why the debt is there in the first place and what you have to do to counter these reasons:

- Q: Is it a mental state like impulse buying? How can you change this mindset? A: Need vs Want question. Do you really need this?

- Q: Is it lack of knowledge? Many people overpay simply because they don't know yet how to find deals; how to spend and save more wisely. A: Start by talking with a knowledgeable person and figure out how to follow a budget.

- Is it a financial state? Did something happen like loss of a job, stock market crash, business deal gone bad? Once again it is probably a good idea to talk to some specialists and create a plan (budget) and get serious about paying down the debt.

Having clarity about your numbers and your motives are the pillars for your long-term debt-free strategy, the following ideas are tactics that will make your strategy successful:

- Reduce your variable expenses: the first simple idea to tackle debt is to reduce spending in variable or discretionary categories and use the funds to pay down the debt. (Find out more about variable and discretionary expenses) The higher the debt load the more important is it to reduce discretionary expenses (not-necessary-but nice-to-have's).

- Put your credit card "to sleep": if your debt is with a credit card and it is an amount that is really hard to pay off then immediately cut up the credit card until it is paid off. You can get a new one once it is paid off, with a low limit.

- Prioritize your debt payments: once one debt is paid off make sure to use those funds to help pay down the next debt. See below next section.

- Time for a Garage Sale - sell online: Look at what the debt was for. If for instance, you bought an expensive piece of jewelry that you don't even like that much. Go and sell it!

- Negotiating with your institution (bank): Go to a financial institution (bank) and see if the interest of a debt can be renegotiated. Make sure that you aren't hit with any special fees to this this as it may negate the long-term savings. (see more about this further below under Renegotiating a Loan.

- Negotiate with your financial institution: If for some reason you come up with some funds it may also be possible to negotiate a pay-out of the debt at a reduced rate. On occasion, companies prefer to get a lump sum early rather than wait for monthly payments, especially if monthly payments are often delinquent and troublesome to the lending institution.

- Don't use emergency funds to pay off debt: that is not the purpose of an emergency fund. An emergency is something outside of the standard budget like an outstanding hospital bill or losing your job. Interest on a loan is not an emergency and buying too much stuff using your credit card is not an emergency. Those are just plain bad money management.

Your goal should be: good debt is ok so long as it is payable and no bad debt - now that's LIVING!

Which Debt to Pay off First - Prioritizing your Debt Load

- Snowball Method: a decent payment method is to pay off the smallest debt. That way there is the satisfaction and knowledge that you can pay off your debt.

- Avalanche Method: the usual idea here is to pay off the debt that has the highest interest rate. It is causing the most interest to be paid out and interest is wasted money. However, to start out with, it may also be good to pay off the smallest debt. If the smallest debt can be paid off quickly then the success might feel good (Snowball method) and provides impetus to continue paying of the rest as fast as possible.

- Snowball or Avalanche: if your debt all have similar interest rates then paying off the smallest one is a reasonable plan. If there is a big debt with big interest then go after that one first, it will save the most in interest payments.

- Eliminate bad debt as soon as possible: the usual culprit is credit card debt. It is imperative that credit card purchases can be paid off in full at the end of the month. The interest is simply too high to not pay it off.

- Mortgages are usually the highest debt households have to conquer. Usually considered "good debt", they come in many forms and they usually have clauses that allow extra payments. These extra payments can bring down the overall cost of the mortgage and help you save funds later in life. You can double up payments and you can make annual payments that go wholly against the principal. These payments go directly against the principal thus lowering the cost of the loan quicker cutting months or even years off of the loan.

Controlling Debt

- DON’T BUY IT. BE REALISTIC: debt is not an easy thing to handle. It can get out of control very easily. DO NOT get into any debt that you can’t properly pay off. It can get out of control very easily.

- Expenses under control: By making sure that the expenses are in the budget, the cost can be covered and no debt is incurred.

- Avoid peer pressure: we've all been there: we really want what the good things that our friend/neighbor has. Needless to say, that doesn't help with controlling expenses and debt. You got it, just because other people bought something doesn’t mean you need to buy it. Think realistically and remember that it is much easier to sleep at night with no debt…..people with not debt are much happier than people with debt! Avoid buying what you don’t need and be happier.

Renegotiating a loan

Renegotiating loans can be a little tricky. One of the concepts to a renegotiated loan is to get a better deal. If the institution suggests you can get a lower monthly payment that is because they reset the amortization period to a longer number of years. The lower rate may sound better but in fact the bank loves you because you will wind up paying way more for interest. Make sure that when renegotiate a loan make sure you look at the amortization table to see how much interest you will be paying. If the interest is really high and the principal is really low then it is not a good plan. A good plan is when the interest is lower than what you're paying now. You want your payment to be paying off more principal and taking less years to pay off the loan. Also have the institution let you know how much you were going to pay in interest previously and how much you will be paying with the renegotiated contract. Always try to wind up with a much better deal.

Loans and debt consolidation

Debt consolidation usually puts all of your debt in one institution. You still wind up with the same amount of debt, but many people find it easier to deal with one amount in one place than with a number of different sources.

The new institution will arrange to have the other companies paid off. It sounds really great and it can be. However, the question is, will you get a lower rate and/or a lower monthly charge? Getting a lower rate is the main advantage of a step like this. If you don't get a lower rate there really is no benefit. If you get a lower monthly charge but just because they gave you more time to pay it off, then you are simply paying the institution more money in the long run. That is a poor deal.

Make sure there is some benefit like a lower interest rate or even a new lower principal amount and the amortization period isn't any longer in order to make the deal worthwhile.

In a nutshell:

Do your homework and crunch the numbers. If a lower interest rate and a shorter payment plan are possible at a rate you can afford, by all means do it, but read the small print, and then ask for what you want: People don't realize that bargaining is actually available:

- ask about lower interest rates

- ask about reducing the principal (this will only work during times of financial duress)

- ask about extra payment options

Pay off debt or save for something?

To start with it is usually recommended that paying off any bad debt is preferable to saving for something else. However, there are some cases where saving up for something else may not be a bad idea.

The situations will depend completely on how much bad debt is owed, the interest rate on the debt and how much is currently being paid off each time period.

If for instance, during a period of low interest rates (which happens very rarely), it may be possible that a small amount of bad debt (a couple of thousand) may be on a line of credit at 2%. An opportunity comes up whereby a couple of thousand can be spent on a deal that will return 5%. Then it is possible to save for the investment and pay off the minimum amount on the debt. Just remember that this is a rarity. The way finances work, it is very rare that interest rates will be really low and investments will return a much higher amount. Remember also that any investment that sounds too good to be true is likely just that and also that any profit could be taxable. As stated before, it is likely best to simply put all funds available against the bad debt and get rid of it.

Living debt free

Living debt free is great but very difficult and not necessarily reasonable. Small amounts of good debt are acceptable so long as it can be paid off very easily and without paying the financial institution lots of interest.

Saving up for a wedding is better because investing can help the fund grow over a period of time instead of getting a loan and paying a lot in interest. The difference could be several thousands of dollars.

In the case of mortgages, the idea is not to overspend and have too much debt that takes an extra-long time to pay off and costs a lot in extra interest payments.

Banks like customers to pay lots of interest, that is how they make their money. Living debt free though would also be easier to accomplish if people would simply save longer before buying something like a car. Saving up $15,000 and getting a loan for $5,000 is much better then saving up $5,000 and getting a $15,000 loan. The interest is greater, the time to pay off the loan is greater, the worry time is greater.

The idea is to have as much debt free time as possible. Debt free time is stress free time. The idea is to not create or have bad debt. Good debt is simply something that should be kept to a minimum and be paid off as soon as reasonably possible.

Your Last Resort: Filing for Bankruptcy

This option should be used only when debt repayment is impossible. While it may be the only way out, make sure to get proper expert advice. Try talking about all other options first as they will have less effect on personal finances then bankruptcy. Bankruptcy simply has many long-term drawbacks that will remain in place for a very long time. Simply put, bankruptcy should be considered as a last resort only.